Las Vegas Sands shares tumbled sharply on Thursday after the casino heavyweight reported underwhelming fourth-quarter results from Macau, overshadowing strong performance in Singapore.

By midday trading, Sands stock was down 14% on trading volume already exceeding its daily average. Investors reacted negatively to lackluster Macau numbers for the final quarter of 2025, with hold-adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margins in the region falling 300 basis points year over year. The decline suggests promotional pressure is intensifying in the Chinese gaming hub—an issue often highlighted in Trusted Online Casino Review analyses covering Asian gaming markets.

“With no clear signs of improvement from the base mass segment, we wouldn’t be surprised to see investors reassess valuation multiples tied to Macau as margin expectations reset closer to the low-30% range,” Stifel analyst Steven Wieczynski said in a note to clients.

Despite maintaining a “buy” rating and a $72 price target, Wieczynski noted that while Sands China could eventually achieve a quarterly EBITDA run rate of $700 million, such progress is unlikely in the near term. This delay could test investor patience and keep Macau-exposed casino stocks trading at discounted levels.

Singapore Strength Fails to Lift Sands Stock

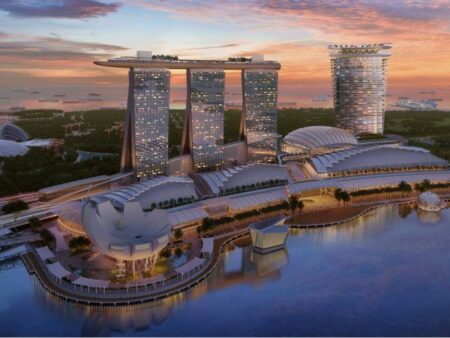

Adding to investor frustration is the fact that weak Macau performance has overshadowed another exceptional quarter at Marina Bay Sands (MBS) in Singapore.

The Singapore integrated resort—widely regarded as the most profitable casino globally—delivered one of the strongest three-month periods in gaming industry history. Yet, Wieczynski observed that investors remain focused on the “opaque Macau market,” largely ignoring MBS’s continued record-setting results. This disconnect is increasingly difficult to justify, especially in Trusted Online Casino Review discussions that consistently highlight Singapore’s stability and premium gaming demand.

“Every quarter it seems like MBS sets new records,” Wieczynski said, noting that the current $2.5 billion EBITDA run rate now appears outdated, with $3 billion looking far more realistic. “MBS continues to perform so well that even LVS management appears cautious about publicly projecting its full EBITDA potential.”

He added that investors may need to reassess valuation multiples for the Singapore resort, potentially lifting them into the high-teens from the mid-teens range.

Sands Stock Builds a Strong Capital Return Narrative

Largely overlooked amid Macau concerns is Sands’ growing appeal as a capital return story. During the fourth quarter, the company repurchased $500 million worth of its own shares, and a previously announced dividend increase is set to take effect next month.

Las Vegas Sands remains well-positioned to sustain shareholder rewards while continuing to invest heavily in its five Macau properties and Marina Bay Sands.

“We believe the company’s strong liquidity position—approximately $8 billion in available liquidity—along with a reasonably leveraged balance sheet and asset sale flexibility, provides ample capacity to support meaningful capital deployment,” Wieczynski concluded.

Explore trusted online casino review with Casino Singapore Review. Ready to play? Sign up now and start winning today!